Last updated: June 2026 | Reading time: ~12 minutes | By the Multicalify Finance Team

Fha vs conventional loan calculator usa helps home buyers compare mortgage options, down payments, PMI, and monthly payments in the United States. Buying a home in 2026 means navigating one of the most consequential financial decisions of your life and the loan type you choose can mean the difference of tens of thousands of dollars over the life of your mortgage. Whether you’re a first-time buyer in Texas, upsizing in California, or refinancing in Florida, understanding FHA vs conventional loans is the foundation of smart home buying.

This guide walks you through everything you need to know: how to use a mortgage calculator, exactly how FHA and conventional loans differ, what you’ll pay in PMI or MIP, and state-specific examples so you can see real numbers not just theory.

Quick Answer: FHA loans suit buyers with lower credit scores (580+) and smaller down payments (3.5%). Conventional loans are better for buyers with strong credit (720+) and 10–20% down, saving money long-term. Use our free US Mortgage Calculator to run your exact numbers in seconds.

Table of Contents

1. What Is a Mortgage Calculator and Why You Need One in 2026

A mortgage calculator is a digital tool that estimates your monthly home loan payment based on the home price, down payment, interest rate, and loan term. In 2026, with US mortgage rates fluctuating between 6.5% and 7.5% depending on loan type and creditworthiness, even a 0.25% difference in your rate can translate to over $15,000 in additional interest on a $400,000 loan.

Here’s why using a mortgage calculator before speaking to a lender is so important:

- You’ll understand your budget ceiling before falling in love with a home above your means

- You can compare FHA vs conventional loan payments side by side in real time

- You’ll spot the true cost of PMI and MIP, which lenders sometimes downplay

- You can model different down payment scenarios (3.5%, 5%, 10%, 20%)

- You avoid being surprised by the difference between your pre-approval amount and your actual comfortable monthly payment

Try it now: Use our free Mortgage Calculator to get your estimated monthly payment in under 60 seconds.

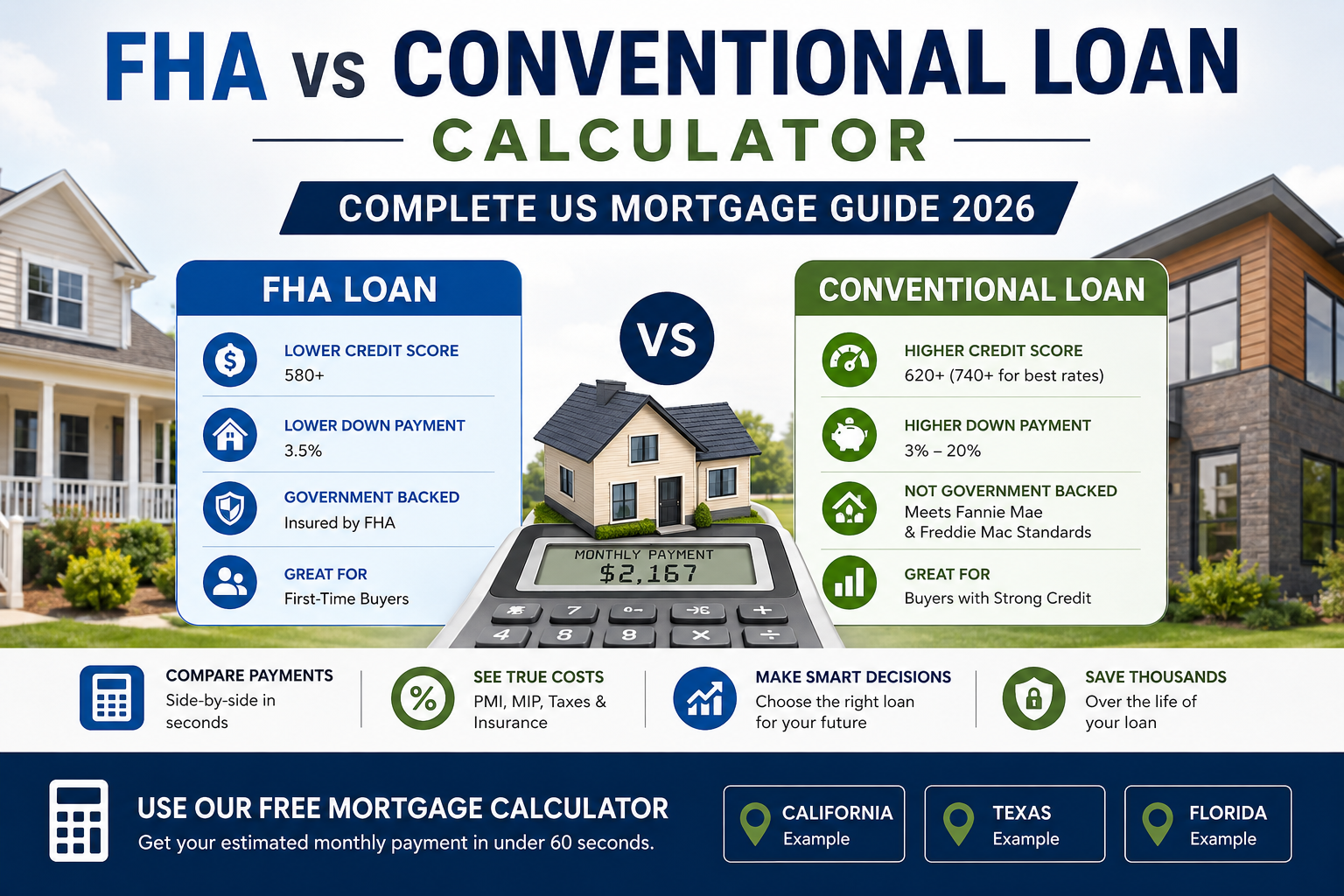

2. FHA vs Conventional Loans: Key Differences Explained

What Is an FHA Loan?

An FHA loan (Federal Housing Administration loan) is a government-backed mortgage insured by the US federal government. Because the government assumes the lending risk, banks and mortgage companies can offer these loans to borrowers with lower credit scores and smaller down payments than they typically would for a conventional loan.

FHA loans are ideal for:

- First-time homebuyers with limited credit history

- Borrowers with credit scores between 580–679

- Buyers who only have 3.5% saved for a down payment

- Those who have had past financial difficulties such as bankruptcy (if at least 2 years ago)

Key FHA loan facts for 2026:

- Minimum credit score: 580 for 3.5% down; 500 for 10% down

- Minimum down payment: 3.5%

- Upfront mortgage insurance premium (UFMIP): 1.75% of loan amount

- Annual MIP: 0.55%–1.05% depending on loan term and LTV

- Debt-to-income (DTI) ratio limit: typically 43%–57% with compensating factors

- 2026 FHA loan limits: $524,225 (floor) to $1,209,750 (ceiling, high-cost areas)

What Is a Conventional Loan?

A conventional loan is a mortgage that is not backed by the federal government. These loans meet the standards set by Fannie Mae and Freddie Mac and are the most common mortgage type in the US. Because there’s no government guarantee, lenders require stronger financial profiles from borrowers.

Conventional loans are ideal for:

- Borrowers with credit scores of 620 or higher (ideally 740+)

- Buyers who can put down 10%–20% or more

- Homebuyers who want to avoid lifetime mortgage insurance costs

- Buyers purchasing higher-priced homes above FHA limits

Key conventional loan facts for 2026:

- Minimum credit score: 620 (most lenders); 740+ for best rates

- Minimum down payment: 3% (for eligible first-time buyers) or 5% standard

- PMI required: Yes, if down payment is below 20%

- PMI rate: typically 0.2%–2% of loan amount annually

- PMI removal: when LTV reaches 80% (you can request) or 78% (automatic)

- 2026 conforming loan limit: $806,500 for most counties; up to $1,209,750 in high-cost areas

3. How to Use the US Mortgage Calculator (Step-by-Step)

Our Mortgage Calculator is designed to be straightforward. Here’s how to get the most out of it:

Step 1: Enter the Home Purchase Price

Type in the full purchase price of the home. For example, if you’re looking at a $450,000 home in Austin, Texas, enter $450,000. If you’re unsure, use the median home price in your target area as a starting point. As of mid-2026, the US median home price is approximately $420,000 according to the National Association of Realtors (NAR).

Step 2: Enter Your Down Payment

Enter either a dollar amount or a percentage. Key thresholds to test:

- 3.5% minimum for FHA loans (credit score 580+)

- 5% common entry point for conventional loans

- 10% significantly reduces PMI costs on conventional loans

- 20% eliminates PMI entirely on conventional loans

Need help figuring out how much you can afford? Use our Loan Calculator to model your borrowing power based on your income.

Step 3: Enter the Interest Rate

In 2026, expect rates roughly in these ranges based on loan type and credit score:

- FHA 30-year fixed: 6.75%–7.25% (average credit)

- Conventional 30-year fixed: 6.5%–7.0% (good credit, 720+)

- Conventional 15-year fixed: 5.9%–6.4% (good credit)

For the most current rates, check Freddie Mac’s Primary Mortgage Market Survey, updated weekly.

Step 4: Select Your Loan Term

Most buyers choose between 15-year and 30-year loans:

- 30-year: Lower monthly payment, more interest paid over life of loan

- 15-year: Higher monthly payment, dramatically less total interest, builds equity faster

Step 5: Add Taxes, Insurance & PMI/MIP

For a realistic total monthly payment, include:

- Property taxes: Varies by state (0.3% in Hawaii to 2.5% in New Jersey annually)

- Homeowner’s insurance: Typically $100–$250/month depending on location and coverage

- PMI or MIP: Add manually based on your loan type (see Section 4 below)

Step 6: Compare Results

Run the calculator twice once with FHA parameters and once with conventional parameters and compare the monthly payments and total costs over 5, 10, and 30 years. This side-by-side view often makes the best choice immediately clear.

Pro tip: Also try our EMI Calculator for a quick monthly installment estimate, and our Loan Calculator to check if the loan amount fits your income.

4. Understanding PMI vs MIP: The Hidden Cost of Your Mortgage

One of the most overlooked costs in homeownership is mortgage insurance and it can add hundreds of dollars to your monthly payment. The type you pay depends on your loan.

Private Mortgage Insurance (PMI) Conventional Loans

PMI protects the lender (not you) if you default on a conventional loan with less than 20% down. PMI is typically added to your monthly payment and ranges from 0.2% to 2.0% of your loan amount annually, depending on your:

- Credit score

- Loan-to-value (LTV) ratio

- Loan term

- Whether the loan is fixed or adjustable

Example: On a $380,000 conventional loan with a 720 credit score and 10% down, PMI might cost around 0.5% annually, or about $158/month. Once your equity reaches 20%, you can request PMI removal saving $1,900+ per year.

How to eliminate PMI faster:

- Make extra principal payments to build equity quicker (use our Mortgage Calculator to model this)

- Request a new home appraisal if your property value has increased significantly

- Refinance once you reach 20% equity

Mortgage Insurance Premium (MIP) FHA Loans

MIP is the FHA equivalent of PMI, but it works differently and often costs more long-term. FHA MIP comes in two parts:

- Upfront MIP (UFMIP): 1.75% of the loan amount, paid at closing (or rolled into the loan). On a $350,000 loan, that’s $6,125 upfront.

- Annual MIP: 0.55%–1.05% of the loan balance, divided into monthly payments.

Critical FHA MIP rule: For FHA loans with less than 10% down, MIP is required for the entire loan term meaning you pay it for 30 years unless you refinance into a conventional loan once you have 20% equity. For FHA loans with 10%+ down, MIP falls off after 11 years.

This lifetime MIP requirement is the number-one reason many financial advisors recommend refinancing from FHA to conventional once you’ve built sufficient equity and improved your credit score.

5. FHA vs Conventional Mortgage: Side-by-Side Comparison 2026

| Feature | FHA Loan | Conventional Loan |

|---|---|---|

| Government backed? | Yes (FHA/HUD) | No |

| Minimum credit score | 580 (3.5% down) / 500 (10% down) | 620 (most lenders) / 740+ for best rates |

| Minimum down payment | 3.5% | 3%–5% (20% to avoid PMI) |

| Mortgage insurance | MIP (upfront 1.75% + annual 0.55–1.05%) | PMI (0.2–2.0% annually) if <20% down |

| MIP/PMI duration | Life of loan (<10% down) / 11 years (10%+ down) | Until 80% LTV (can request removal) |

| 2026 loan limits | $524,225 – $1,209,750 | $806,500 – $1,209,750 (conforming) |

| Interest rates (30yr avg, 2026) | 6.75%–7.25% | 6.5%–7.0% (good credit) |

| DTI ratio limit | Up to 57% with strong factors | Up to 45–50% with strong factors |

| Property requirements | Must meet HUD minimum standards | More flexible (no federal standards) |

| Best for | Low credit / low down payment buyers | Strong credit / higher down payment buyers |

Source: HUD, Fannie Mae, Freddie Mac guidelines 2026 values. Always verify current limits with your lender.

Run your numbers: Use our Mortgage Calculator to compare your FHA vs conventional monthly payments with your exact figures.

6. State-Specific Mortgage Examples: California, Texas & Florida (2026)

Mortgage costs vary dramatically by state due to differences in home prices, property taxes, and insurance rates. Here are real-world examples using median 2026 home prices.

California: $750,000 Home Los Angeles Area

California’s high home prices mean many buyers are pushed toward jumbo loans or high-balance FHA loans. The 2026 FHA ceiling for Los Angeles County is $1,089,300.

| Scenario | FHA Loan (3.5% down) | Conventional (10% down) | Conventional (20% down) |

|---|---|---|---|

| Home price | $750,000 | $750,000 | $750,000 |

| Down payment | $26,250 (3.5%) | $75,000 (10%) | $150,000 (20%) |

| Loan amount | $723,750 | $675,000 | $600,000 |

| Interest rate (30yr) | 7.0% | 6.75% | 6.625% |

| Principal & interest | $4,817/mo | $4,378/mo | $3,840/mo |

| MIP/PMI | ~$331/mo (MIP) | ~$281/mo (PMI) | $0 |

| Est. property tax | ~$781/mo (1.25% annual) | ~$781/mo | ~$781/mo |

| Est. total payment | ~$6,129/mo | ~$5,640/mo | ~$4,821/mo |

California takeaway: Even with a lower down payment, the FHA option costs nearly $1,300 more per month than a 20%-down conventional loan. If you can stretch to 20% down on a California home, the long-term savings are substantial. Use our Mortgage Calculator to run your specific California scenarios.

Texas: $380,000 Home Austin/Dallas Area

Texas has no state income tax but some of the highest property taxes in the US (average ~1.8%–2.2% annually), which significantly affects total mortgage costs.

| Scenario | FHA Loan (3.5% down) | Conventional (10% down) | Conventional (20% down) |

|---|---|---|---|

| Home price | $380,000 | $380,000 | $380,000 |

| Down payment | $13,300 (3.5%) | $38,000 (10%) | $76,000 (20%) |

| Loan amount | $366,700 | $342,000 | $304,000 |

| Interest rate (30yr) | 7.0% | 6.75% | 6.625% |

| Principal & interest | $2,441/mo | $2,218/mo | $1,946/mo |

| MIP/PMI | ~$168/mo (MIP) | ~$143/mo (PMI) | $0 |

| Est. property tax | ~$633/mo (2.0% annual) | ~$633/mo | ~$633/mo |

| Est. total payment | ~$3,392/mo | ~$3,144/mo | ~$2,779/mo |

Texas takeaway: Property taxes add over $600/month in Austin buyers often underestimate this. Even with a lower mortgage payment from a big down payment, your Texas total housing cost will be notably higher than in lower-tax states.

Florida: $420,000 Home Miami/Tampa Area

Florida’s insurance costs have surged in recent years due to hurricane risk. Homeowner’s insurance can run $3,000–$6,000+ annually in South Florida, adding $250–$500/month to your housing costs.

| Scenario | FHA Loan (3.5% down) | Conventional (10% down) | Conventional (20% down) |

|---|---|---|---|

| Home price | $420,000 | $420,000 | $420,000 |

| Down payment | $14,700 (3.5%) | $42,000 (10%) | $84,000 (20%) |

| Loan amount | $405,300 | $378,000 | $336,000 |

| Interest rate (30yr) | 7.0% | 6.75% | 6.625% |

| Principal & interest | $2,699/mo | $2,452/mo | $2,151/mo |

| MIP/PMI | ~$186/mo (MIP) | ~$158/mo (PMI) | $0 |

| Property tax + insurance | ~$700/mo (1.0% tax + insurance) | ~$700/mo | ~$700/mo |

| Est. total payment | ~$3,585/mo | ~$3,310/mo | ~$2,851/mo |

Florida takeaway: Don’t underestimate insurance. Florida homebuyers should get insurance quotes before making an offer some properties in flood zones require separate flood insurance on top of homeowner’s insurance.

For all three states, use our free Mortgage Calculator to enter your exact figures and get a personalized breakdown.

7. Related Financial Calculators to Complete Your Home-Buying Picture

Mortgage payments are just one piece of the financial puzzle. Here are the calculators you should use alongside our mortgage tool to make the most informed decision:

- Loan Calculator Calculate whether you qualify for your target loan amount based on income and existing debts

- EMI Calculator Get a quick monthly installment estimate for any loan amount and term

- SIP / Investment Calculator Compare renting + investing vs buying: what would your down payment grow to if invested instead?

- Financial Health Check Just as you track your physical health, track your financial health with our suite of tools

- Salary Increase Calculator Understand how a raise affects your mortgage affordability and DTI ratio

For broader home-buying research, these external resources are trusted industry standards:

- Consumer Financial Protection Bureau (CFPB) — Owning a Home

- HUD.gov — Buying a Home Guide

- Freddie Mac — Weekly Mortgage Rate Survey

- National Association of Realtors — Housing Statistics

8. Frequently Asked Questions

What is the minimum down payment for an FHA loan in 2026?

The minimum down payment for an FHA loan in 2026 is 3.5% of the purchase price, provided your credit score is 580 or higher. If your score is between 500–579, you must put down at least 10%. On a $380,000 home, 3.5% down equals $13,300 significantly less than the $76,000 needed for a 20% conventional down payment.

What credit score do I need for a conventional loan?

Most lenders require a minimum credit score of 620 for a conventional loan. However, a score of 740 or above will secure you the best interest rates and eliminate the PMI surcharge on rates. Each 20-point score improvement can lower your rate by 0.125%–0.25%, which adds up to thousands in savings over 30 years.

How much is FHA mortgage insurance in 2026?

FHA loans require two types of mortgage insurance in 2026: an upfront MIP of 1.75% of the loan amount (added at closing or rolled into the loan), plus an annual MIP of 0.55%–1.05% depending on your loan term, amount, and LTV ratio. For a $350,000 loan, this means roughly $6,125 upfront plus around $160–$306/month ongoing.

When can I remove PMI from a conventional loan?

You can request PMI removal on a conventional loan once your equity reaches 20% (LTV of 80%). Under the federal Homeowners Protection Act, your lender must automatically cancel PMI when your LTV reaches 78% based on the original amortization schedule. You can accelerate this by making extra principal payments try our Mortgage Calculator to see how much faster you can build equity.

Is an FHA loan or conventional loan better for first-time buyers?

It depends on your credit score and savings:

- FHA is usually better if your credit score is 580–679 or you only have 3.5%–5% saved for a down payment

- Conventional is usually better if your credit score is 720+ and you can put down 10%–20%, because you’ll avoid lifetime MIP costs and likely get a lower interest rate

Many financial advisors suggest starting with an FHA loan if needed, then refinancing to conventional once your equity and credit score improve typically within 3–7 years.

What are the 2026 FHA loan limits?

The 2026 FHA loan limits vary by county. For most US counties, the floor (minimum limit) is $524,225 for a single-family home. In high-cost areas including San Francisco, Los Angeles, New York City, and Seattle, the ceiling reaches $1,209,750. Alaska, Hawaii, Guam, and the US Virgin Islands have even higher limits. Check your county’s exact FHA limit at HUD.gov.

Can I use a mortgage calculator for refinancing?

Absolutely. Simply enter your remaining loan balance as the “loan amount,” your current home value to determine LTV, and the new interest rate you’ve been quoted. Compare the output to your current monthly payment to determine if refinancing makes financial sense. Generally, refinancing is worth it if you can lower your rate by 0.75%+ and plan to stay in the home for at least 3–4 more years to recoup closing costs. Use our Mortgage Calculator to model refinance scenarios.

9. Conclusion: Which Mortgage Loan Is Right for You in 2026?

The FHA vs conventional decision comes down to three things: your credit score, your down payment amount, and how long you plan to stay in the home.

Choose FHA if:

- Your credit score is 580–679

- You have less than 10% for a down payment

- You’re buying in an area within FHA loan limits

- You need flexible debt-to-income ratio qualification

Choose Conventional if:

- Your credit score is 720 or above

- You can put down 10% or more (especially 20% to eliminate PMI)

- You’re buying a higher-priced home above FHA limits

- You want to avoid lifetime mortgage insurance costs

The best next step is to run your specific numbers. Our free US Mortgage Calculator lets you model both scenarios in minutes no sign-up required.

Have questions or want help interpreting your results? Drop a comment below or explore our full suite of finance calculators to build a complete picture of your financial health before making one of the biggest decisions of your life.

Disclaimer: The figures in this article are estimates based on average 2026 rates and are for educational purposes only. Actual mortgage payments, rates, and insurance costs will vary based on your lender, credit profile, location, and market conditions. Always consult with a licensed mortgage professional before making financial decisions. Multicalify is not a mortgage lender or financial advisor.